Until the introduction of the Corporate Sustainability Reporting Directive (CSRD), European companies could freely choose which standard to refer to when reporting their ESG performance. In the absence of binding guidelines, the most widely used standard was GRI – Global Reporting Initiative, internationally recognised for its comprehensive structure and ESG impact orientation.

However, the voluntary approach led to significant heterogeneity in reports: each company followed different frameworks (GRI, SASB, CDP, TCFD, etc.), making it difficult to compare data and thus assess the sustainability efforts objectively, in order to achieve the common goal of improving ESG performance.

Why a new standard was needed: Introduction of the ESRS

The main limitation of the wide variety of reporting standards was the lack of comparability of information and data. Companies reported in different ways, making it difficult to assess impacts, strategies, and performance. Meanwhile, pressures from investors and banks grew, demanding reliable, comparable, and verifiable ESG information. This created the need for a common, clear, and regulated language.

What are the ESRS

The ESRS (European Sustainability Reporting Standards) are the European Standards for Sustainability Reporting, developed by EFRAG (European Financial Reporting Advisory Group) under the mandate of the European Commission. They serve as the technical and regulatory reference for sustainability reporting required by the CSRD.

The main goal of the ESRS is the standardisation and comparability of environmental, social, and governance (ESG) information reported by European companies, improving transparency, reliability, and traceability of sustainability data.

Key Highlights of the ESRS

- Mandatory: The ESRS is mandatory for all companies subject to the CSRD (large companies and, progressively, listed SMEs). The goal is to extend sustainability transparency to a much wider range of companies compared to the past.

- Double Materiality: Information must be selected according to the principle of double materiality (impact materiality and financial materiality). Companies must therefore integrate sustainability into risk management and business strategy, not treat it as an external or ancillary element.

- Interoperability: The ESRS is aligned with other international standards, such as those from the Global Reporting Initiative (GRI), ISSB (IFRS), and Task Force on Climate-related Financial Disclosures (TCFD). This interoperability acts as a bridge between European and international reporting, strengthening the credibility of the European single market.

- Stakeholder-Inclusive Approach and Value Chain: The ESRS requires active engagement with relevant stakeholders (both internal and external) and extending reporting across the entire value chain. This approach enables the assessment of systemic impacts and promotes a more responsible and forward-looking view of economic activity.

- Digitalisation: Reporting will also be digital and structured, using the XBRL (eXtensible Business Reporting Language), which is already adopted in the financial reporting domain.

The European Sustainability Reporting Standards (ESRS) represents a structured framework for the reporting of sustainability information by companies, divided into four key areas: cross-cutting standards, environment, social, and governance.

- The cross-cutting standards establish general principles and reporting requirements, ensuring consistency and comparability across companies.

- The environment section delves into critical topics such as climate change, pollution, the use of water and marine resources, biodiversity, and the circular economy, helping organizations measure and manage their ecological impact..

- The social area focuses on the internal workforce, workers in the value chain, affected communities, and consumers, highlighting the role of sustainability in business relationships.

- Finally, the governance section addresses business conduct, ensuring transparency and accountability in managing ESG issues.

This reporting system, made mandatory by the Corporate Sustainability Reporting Directive (CSRD), ensures that European companies provide detailed and standardized information, facilitating the comparability and evaluation of their sustainability performance.

The Materiality Analysis process

To conduct a robust and credible materiality analysis, five key phases:

- Structure an appropriate governance process

- Define a universe of material issues

- Collect data and evidence to support the analysis

- Act on the results of the analysis

- Monitor the evolution of materiality over time

A crucial element of the process is stakeholder engagement, as they must be consulted on both impact-related and financial issues. However, their opinion should not be the only basis for the analysis.

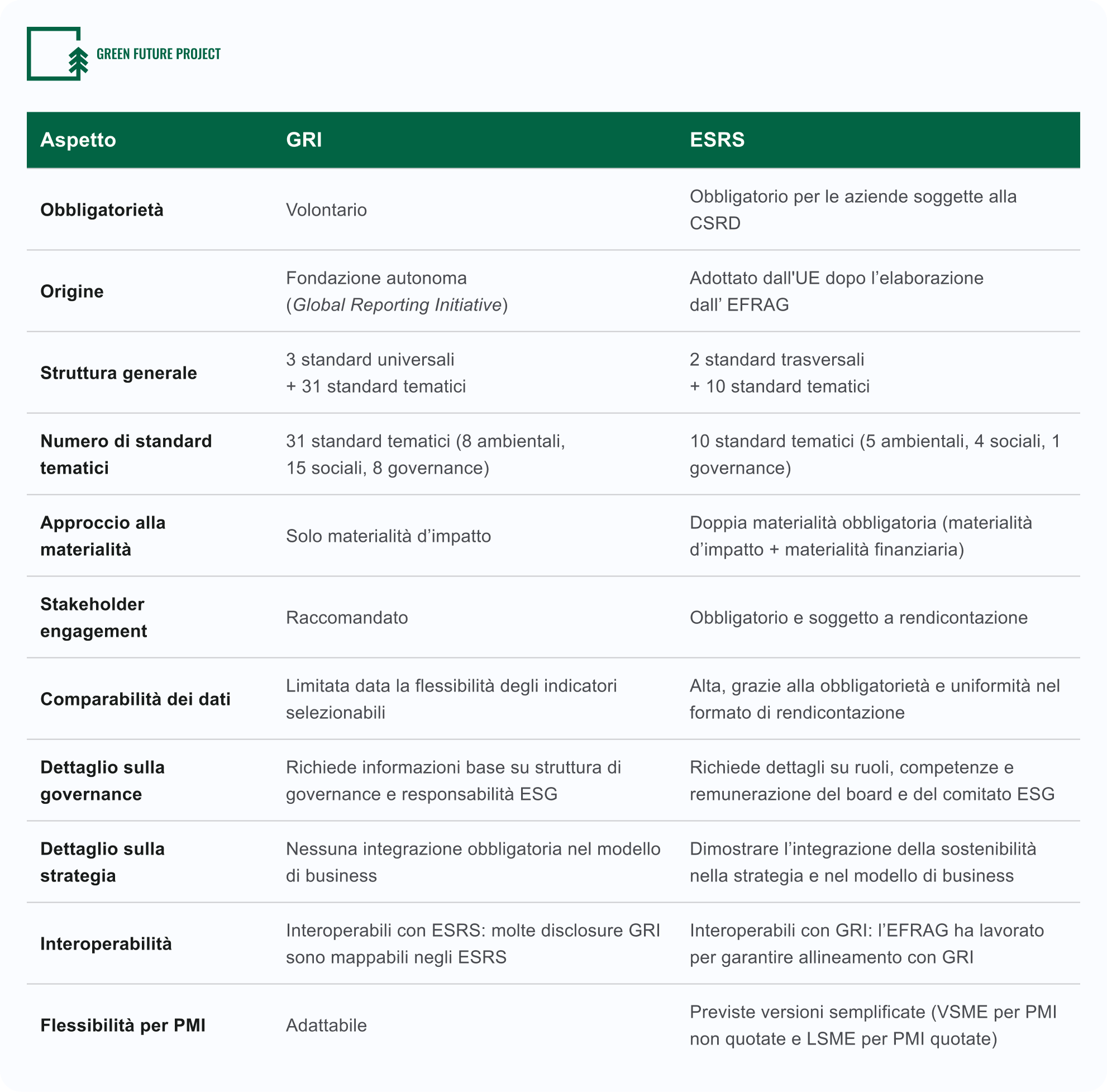

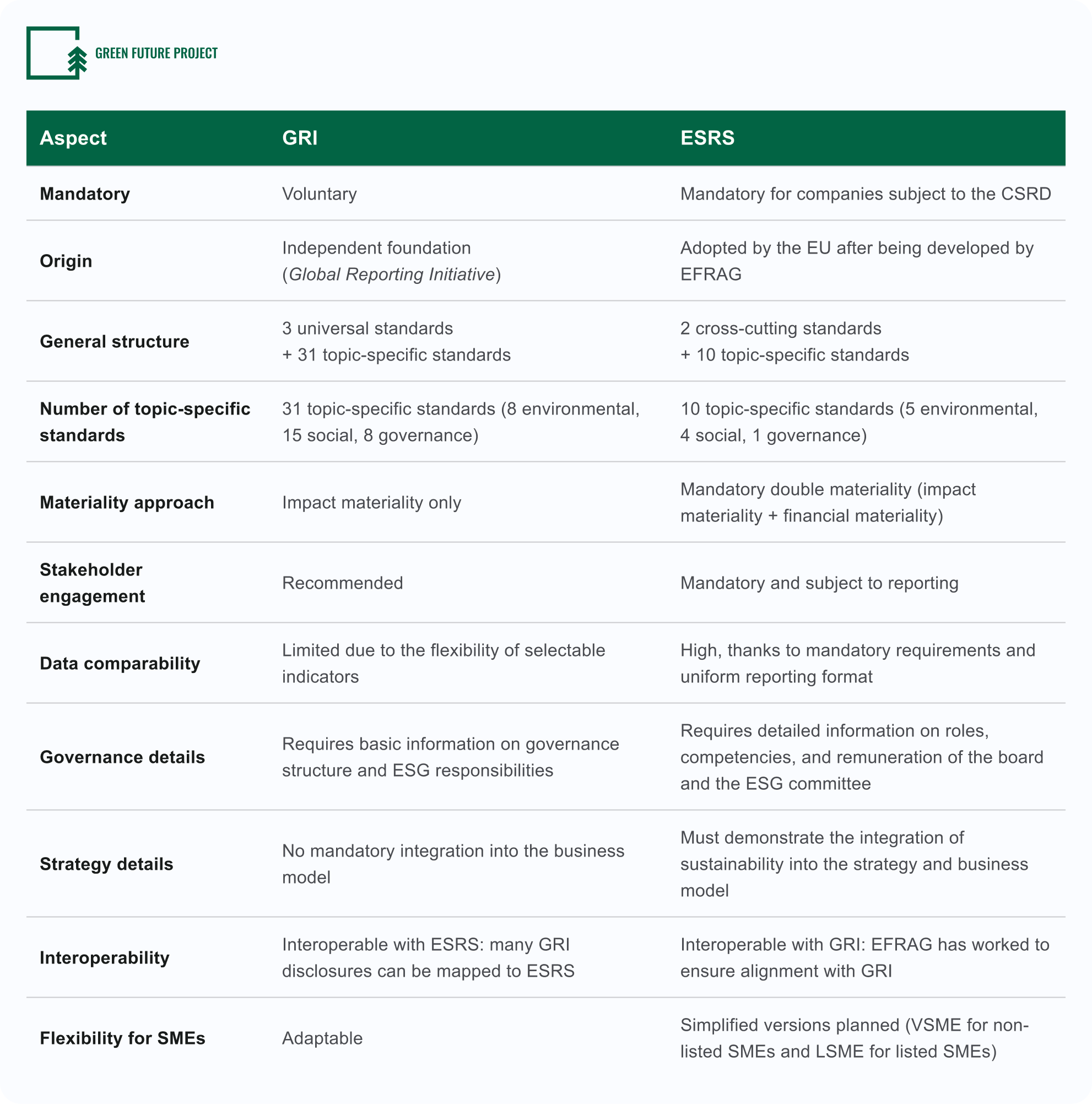

Comparative Table between GRI and ESRS

{kind=link}